Supermarket chain Lopia leaps from cash-only to cashless payments via its own payment system

With distributors and retailers also expected to get on board with the shift to cashless payments, spring 2025 saw supermarket chain Lopia abandon its cash-only payment policy to introduce a proprietary cashless payment system.

Lopia brought in the new system in just three months—a lightning shift that was actually underpinned by a five-year history of SMBC support.

To find out more about the background behind this shift and the road ahead, we talked with Yohei Funai, Director of SoupStream—the company handling the digitalization of Lopia operator OIC Group and also involved in building Lopia’s cashless payment system—along with Yo Inoue and Iori Miwa, respectively Head and Deputy General Manager of the Transaction Business Promotion & Planning Team within the Transaction Banking Department in SMBC’s Transaction Business Division, which handled support for the transition.

- First step away from cash-only to cashless payments while minimizing store burden

- Bank Pay’s multi-bank reach enables a one-stop approach—regional banks included

- Close collaboration feeds five years of planning into a three-month rollout

- App design carefully balances ease of use and security

- Cashless payments and data utilization open the way for a new customer experience

First step away from cash-only to cashless payments while minimizing store burden

How are distribution and retail doing on the transition to cashless payments?

As lifestyles and purchasing behavior change, supermarkets are also being pushed toward cashless payments. Lopia has always had a cash-only policy, but not only is our business scale growing—we’re opening more than 30 new stores a year—but our customer base is becoming increasingly diverse. When you include the imperatives of boosting operational efficiency and enhancing the customer experience, introducing cashless payments was really the only choice. And then, of course, there was the major pull factor of being able to use purchasing data to analyze customer behavior.

There are numerous different payment methods out there—what made you opt for cashless payments via Lopia’s own official app?

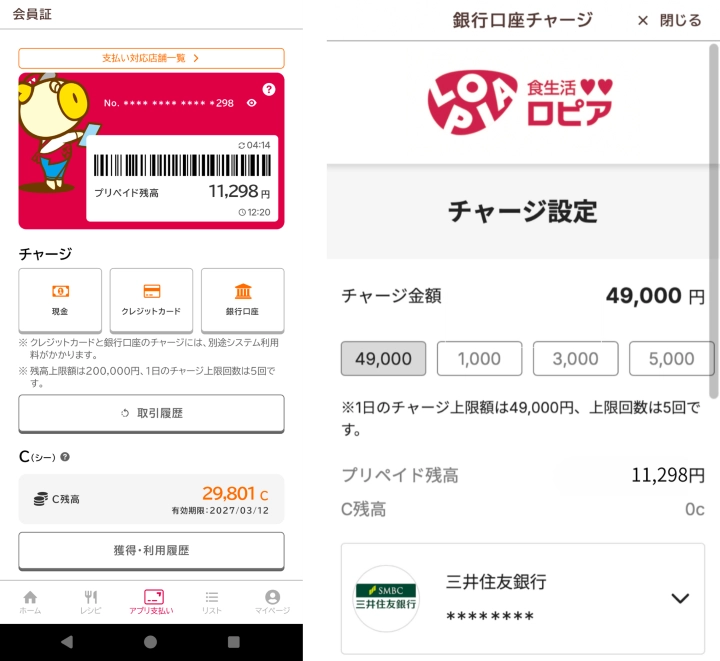

With app-based payments becoming more common and offering more user convenience, we recognized the potential to enhance customer engagement. We also wanted to create a mechanism that wouldn’t interfere with store operations.

Yes, there are many different payment methods available today, but our POS systems vary by store. We wanted a solution that wasn’t tied to any particular POS system and could be implemented simply by changing the software. In terms of a flexible setup that we could implement by just installing read-only terminals or devices that work alongside the existing POS systems, adopting our own payment service made the most sense.

When you were making the cashless transition, how did you go about choosing a partner?

Because integration with Bank Pay* and support for bank-based top-ups were non-negotiable requirements for us, adopting Bank Pay was basically the only option.

* A QR code payment service provided by the Japan Electronic Payment Promotion Organization that enables payments through linkage with a registered bank account.

SMBC is reportedly the No. 1 domestic bank in terms of Bank Pay adoption. What do you believe has enabled SMBC to expand its market share so successfully?

As cashless payments become the mainstream, customer issues and needs continue to change. I think that our success comes down to our consistent, long-term efforts to prepare for and respond to these changes.

Recognizing that some issues can’t be solved by banks alone, we work closely with SMBC Group companies and external partners to build and continually update solutions that address our customers’ issues. This approach has led many customers to choose our services.

In particular, the direct link to bank accounts makes it essential to lock in strong security measures so that users can feel safe using Bank Pay. We identify gaps between the necessary measures and the current state of customers’ services, propose practical measures to close those gaps, and work through them together with the customer.

I think the ability to provide this kind of end-to-end, hands-on support is a unique SMBC strength.

Our involvement doesn’t end with the customer launching their own payment service. To make users more likely to continue to use the service, we provide the customer with data analysis support and work with them to consider next steps based on the analysis results. We then verify the effectiveness of those steps and apply the results to the next phase. I think that SMBC is great at staying with and supporting this ongoing cycle.

Bank Pay’s multi-bank reach enables a one-stop approach—regional banks included

How many banks and credit card companies are partnered with the Lopia payment service?

Transactions can be made with all banks and card companies that accept Bank Pay. That multi-bank reach significantly lowered the hurdles to system implementation. Since Lopia has a nationwide footprint, it’s great to know that the coverage extends even to regional banks. It’s also a major advantage that we can add new partner banks simply by adding their logos to the app screen.

What changes did you see after the nationwide rollout?

There are regional differences, but Kansai has particularly high usage rates and app member numbers. Newer stores tend to have a higher proportion of cashless transactions. Adoption rates are relatively low in older stores where customers’ purchasing habits are already entrenched, but when customers do use cashless payments, the feedback is very positive—like how great it is not to have to carry coins any more. Some of our stores even have customers in their 70s and 80s who are active app users.

Have you seen any changes in per-purchase amounts or shopping frequency?

Per-purchase amounts have definitely increased. We don’t have pre-implementation data on visit frequency, so we can’t run a direct comparison, but customers using cashless payments tend to visit at least once a week and make fewer small-value transactions. Interestingly, we’ve noticed that cashless payments become more convenient and customers make more frequent visits to our stores in areas where there are rival stores nearby.

Close collaboration feeds five years of planning into a three-month rollout

How long did implementation take?

From the initial proposal to the finish, nearly five years. Lopia was seen as the last holdout in the industry, so when the decision was made to go cashless, it sent a bit of a jolt through SMBC. The distribution and retail sector was apparently also buzzing at the news.

We’d been kicking the idea around for a while, but we’d just never gotten it across the line. Then around the end of last year, we came up with a roadmap and stepped on the gas. The actual implementation period was about three months, beginning with a trial rollout in February that expanded nationwide from March to May. Actual, full-scale, nationwide deployment started around September. We began in Kyushu and then expanded to Tohoku and Hokkaido in April and May. Our Kanto stores use a wide range of POS systems, so we held off the whole rollout there for a while to avoid risk.

Why did you start with regional stores?

We have a lot of new stores and a lot of new customers there, so it was easy to have them install the app on the spot and start using the Lopia payment system. We probably wouldn’t have been able to start regionally if Bank Pay hadn’t allowed payments from accounts at a range of banks. Oh, and we launched the trial rollout with a number of stores in the Kanto area so that if any issues arose, we could get straight out there and sort them out.

What made you finally step on the gas last year?

We wanted to set up an environment where customers could make both cash and cashless payments—and we wanted to get everything in place as soon as possible. We also needed to expedite the nationwide rollout from a data analysis standpoint, as well as launching a joint Bank Pay campaign.

Customers have three main ways of topping up their Lopia accounts: cash, bank account, or credit card. In this case, the two companies collaborated to run a campaign limited to top-ups from bank accounts. For Lopia, the goal was to increase usage of both the Lopia member app and payment service, while for us, the aim was to acquire new users topping up via bank accounts and grow transaction volume.

The campaign produced a significant bump in the use of bank account top-ups, and a number of customers continued to use the service even after the campaign ended—so we’ve seen a tangible effect in terms of entrenching the use of Bank Pay.

App design carefully balances ease of use and security

What creative solutions did you come up with when revamping the app and implementing the payment functions?

We knew that Lopia had been operating a cash-only payment system and was very conscious of the costs associated with cashless payments. With that in mind, we set out right from the design stage to maximize the benefits unique to bank account-linked payments by realizing two goals: enhancing the shopping experience for those Lopia customers who really wanted a cashless option and keeping down cashless payment costs in line with Lopia’s strict cost control system.

We put a huge amount of thought into the UI/UX, experimenting over and over with the positioning of every single button and icon. In contrast to the broad approach that we took to the app’s back end, we made a conscious effort to keep the front end familiar to customers who already use cashless apps. The focus was always on the customer perspective rather than our own preferences.

It was pretty challenging to balance the UI/UX that Lopia wanted with Bank Pay’s rigorous security requirements

The greater the focus on ease of use, the more concerns arise around security—and even then you managed to accommodate all our requests!

There was a very close collaborative process among Lopia, SMBC, and the system vendor on everything from security-conscious app design to post-launch user follow-ups, entailing numerous meetings along the way. I think that all the experience and know-how SMBC has gathered over the years was key in enabling discussions to proceed so smoothly toward finding solutions. Having amassed the knowledge that a particular request corresponds to a particular pattern, for example, allowed us to provide seamless support toward implementation.

Cashless payments and data utilization open the way for a new customer experience

It seems like you might also be leveraging purchasing data going ahead?

Until now, we thought about the customer experience only in in-store terms, not paying much attention to pre- and post-purchase behavior. Cashless payments have let us collect purchasing data so that we can finally see the whole picture. In terms of the payment space, this represents both a major turning point and an entry point.

In other words, payments have traditionally been viewed as the final stage in a customer’s purchase journey—the exit point—but from a marketing standpoint, they can actually become an entry point.

SMBC’s strong focus on digitalization has been a great source of learning for us. We plan to analyze the data from the August cashback campaign and leverage insights from actual usage for our next initiatives. We really appreciate SMBC’s unwavering support throughout this whole journey.

To see what would move things forward, we experimented with different approaches and presented various ideas for feedback. The results of that iterative process are what have brought us to where we are today. Looking back at those past proposals, I really sense the passion that the team members were bringing at the time.

I think that of all the banks they could have approached, Lopia chose us because of that accumulation of communication over five years since we first began discussions in 2019.

Finally, what are your plans moving forward?

Payments play a key role in transforming the customer experience, and cashless payments will continue to grow. We want to use payment data to evolve from our previous mass-market approach to one that delivers personalized care to each customer, building a Lopia fan base. We look forward to continuing our close collaboration with SMBC on that journey.

This project has reinforced my view that a proprietary cashless payment service is essentially a redesign of customer touchpoints. While different companies will have different approaches to cashless payments, I hope that as one option they will consider both creating their own cashless payment service and adopting Bank Pay, which combines versatility with strong security. SMBC will continue to work closely with customers, supporting them in resolving management issues from optimizing their cashless payment costs to enhancing user engagement and using data to advance their marketing capabilities.

Team members on both sides have come and gone over the last five years, but it’s their cumulative efforts that have led to today’s results. This project was certainly not something that we pulled off on our own. It’s the product of support and effort from Lopia and many partners inside and outside SMBC. We are sincerely grateful, and we look forward to continuing to offer support, spreading new uses of bank accounts and advancing the adoption of cashless payments throughout the distribution sector.

-

Director, SoupStream Co., Ltd.

Yohei Funai

Joined OIC Group Co., Ltd. in 2024 after scaling digital service business at an information and communications major and in the retail sector. At SoupStream, he leads digital transformation initiatives including app development and cashless payment services.

-

Head of the Transaction Business Promotion & Planning Team, Transaction Banking Department

Transaction Business Division, Sumitomo Mitsui Banking CorporationYo Inoue

Joined SMBC in 2018 after launching and scaling fintech services at a major credit card company and an information and communications company. He has worked on payment services, including Bank Pay, and engaged in infrastructure planning. Currently, he leads transaction business planning for corporate customers.

-

Deputy General Manager, Transaction Business Promotion & Planning Team, Transaction Banking Department, Transaction Business Division, Sumitomo Mitsui Banking Corporation

Iori Miwa

Joined SMBC in 2012. After handling corporate sales for small and mid-sized enterprises in the Corporate Business Office, he moved in January 2015 to the Payment and Settlement Operations Department (now the Transaction Banking Department), where he is responsible for sales promotion and planning with a focus on transaction banking business.