3. Resolving the non-performing loan issue under challenging business conditions

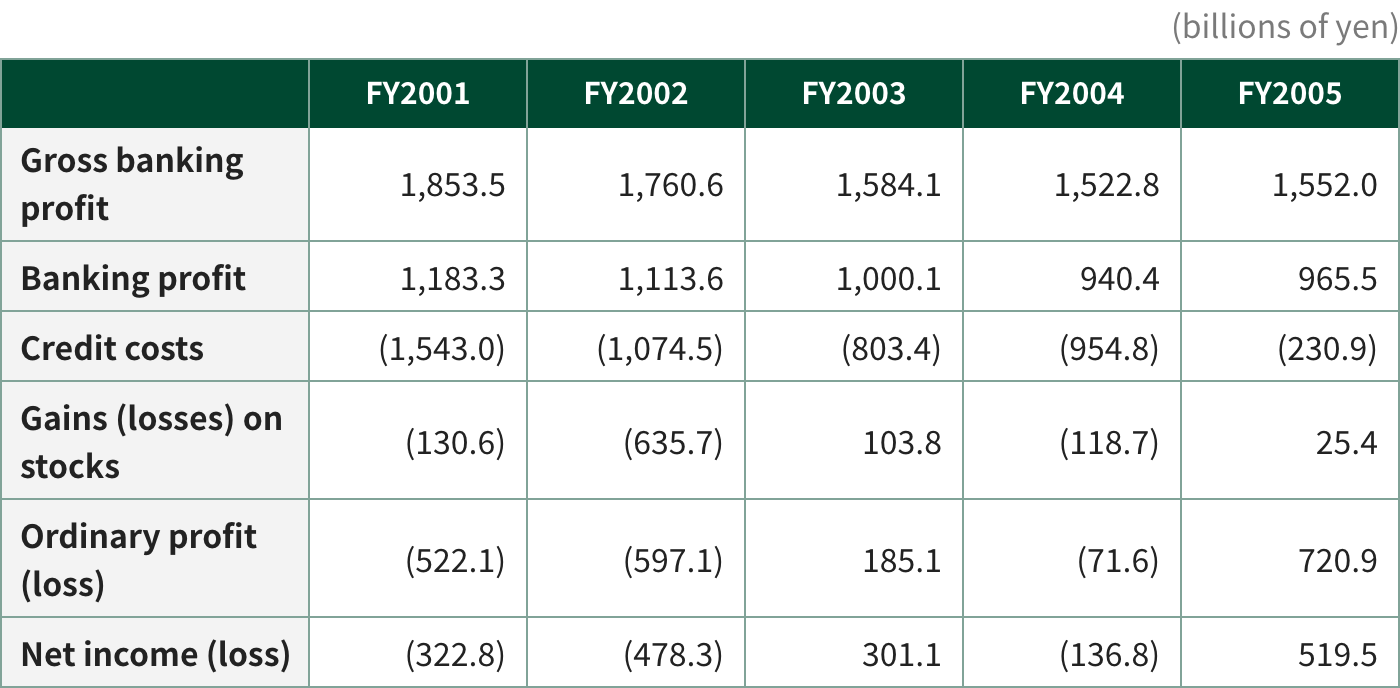

For the first two years after the merger in fiscal years 2001 and 2002 (ended March 2002 and March 2003), SMBC posted more than one trillion yen in banking profit for each year, owing to successful efforts to increase earning capacity and cost efficiency. However, this achievement was more than offset by increased credit costs (the total amount of costs related to writing off loans, especially disposition of non-performing loans, and the provision for a general reserve for possible loan losses) and losses due to a decline in stock prices, resulting in sizable net losses for two consecutive years. This, in turn, brought about a consolidated net loss posted by SMFG for the fiscal year 2002 in the first earnings report of the company launched in December 2002. In August 2003, SMFG received an order for business improvement from the Financial Services Agency due to the business results, which fell notably short of the targets that had been set pursuant to a plan aiming to strengthen the business base, and whose results were gauged by measuring profits.

In the fiscal year 2003, SMBC reported banking profit of over one trillion yen, which more than offset credit costs of 803.4 billion yen to achieve 301.1 billion yen in net income, allowing the business to attain profitability for the first time after its establishment. In the following fiscal year 2004, however, both SMBC (non-consolidated) and SMFG (consolidated) posted net losses, returning to unprofitability, due to banking profit declining to less than one trillion yen, partly reflecting a reactionary fall in income from the Treasury Unit and 954.8 billion yen of credit costs. This resulted in SMFG receiving a second order for business improvement from the Financial Services Agency.

-

Chapter 1The Financial Crisis and Realignment of the Financial Sector

-

Chapter 2The Birth of SMBC and SMFG

-

Chapter 3Initiatives Pursued by SMBC Banking Units in the Early Years

-

Chapter 3Initiatives Pursued by SMBC Banking Units in the Early Years

-

- Enhancing our retail consulting and payments & consumer finance businesses

- Enhancing corporate financial solutions

- Banking-Securities collaboration in the wholesale securities business

- Challenges facing our global banking business

- Actions by Treasury Unit in preparation for rising interest rates

- Integration of operating systems and administrative functions

-

-

-

Chapter 4Embarking on Fresh Challenges Under New Leadership

-

Chapter 4Embarking on Fresh Challenges Under New Leadership

-

- Changes of leadership and the announcement of our new management policy

- Developing group business strategies

- Addressing antitrust issues

- Completing repayment of public funds

- LEAD THE VALUE

- Enhancing our retail financial consulting business

- Enhancing our corporate solution business

- Enhancing our investment banking business

- Global banking business turnaround

- Upgrading risk management in preparation for Basel II

- Development of human resources

- CSR activities

-

-

-

Chapter 5SMFG’s Response to Global Economic and Financial Turmoil

-

Chapter 6Preparing for the Next Decade

-

Chapter 1Business Model Reform Under Challenging Business Conditions

-

Chapter 1Business Model Reform Under Challenging Business Conditions

-

- Our journey under new leadership (the second decade)

- Focusing on growth industries and businesses

- Reforming domestic business operations

- Promoting banking-securities collaboration in Wholesale Banking Unit

- Structural reform of our retail business

- Meeting the needs of an aging society

- Abenomics and Treasury Unit's nimble portfolio management

- Operating in a negative-interest-rate environment

-

-

-

Chapter 2Enhancing Group Businesses

-

Chapter 3Expanding Our Global Business

-

Chapter 4Enhancing Corporate Infrastructure Under a New Governance Framework

-

Chapter 4Enhancing Corporate Infrastructure Under a New Governance Framework

-

- New leadership and enhancing corporate governance

- Introducing group-wide business units and CxO system

- Improving capital, asset, and cost efficiency

- Pursuing our cashless payment strategies

- Retail branch reorganization

- Customer-oriented business conduct

- Enhancing internal-control frameworks

- Valuing diversity and revision of our HR framework

-

-

-

Chapter 5The Path for Our Future

-

Chapter 6Opening a New Chapter in SMBC Group’s History